AXIOM

I tried to build a daily stock-prediction signal, caught the first version leaking, and rebuilt it carefully. This page shows what's left after a clean test: a small signal that loses to just holding the market.

Can daily price and volume data beat buy-and-hold?

Short version: the model finds a tiny positive signal, but it loses to just holding the same names and doesn't survive a Sharpe adjustment for how many things I tried.

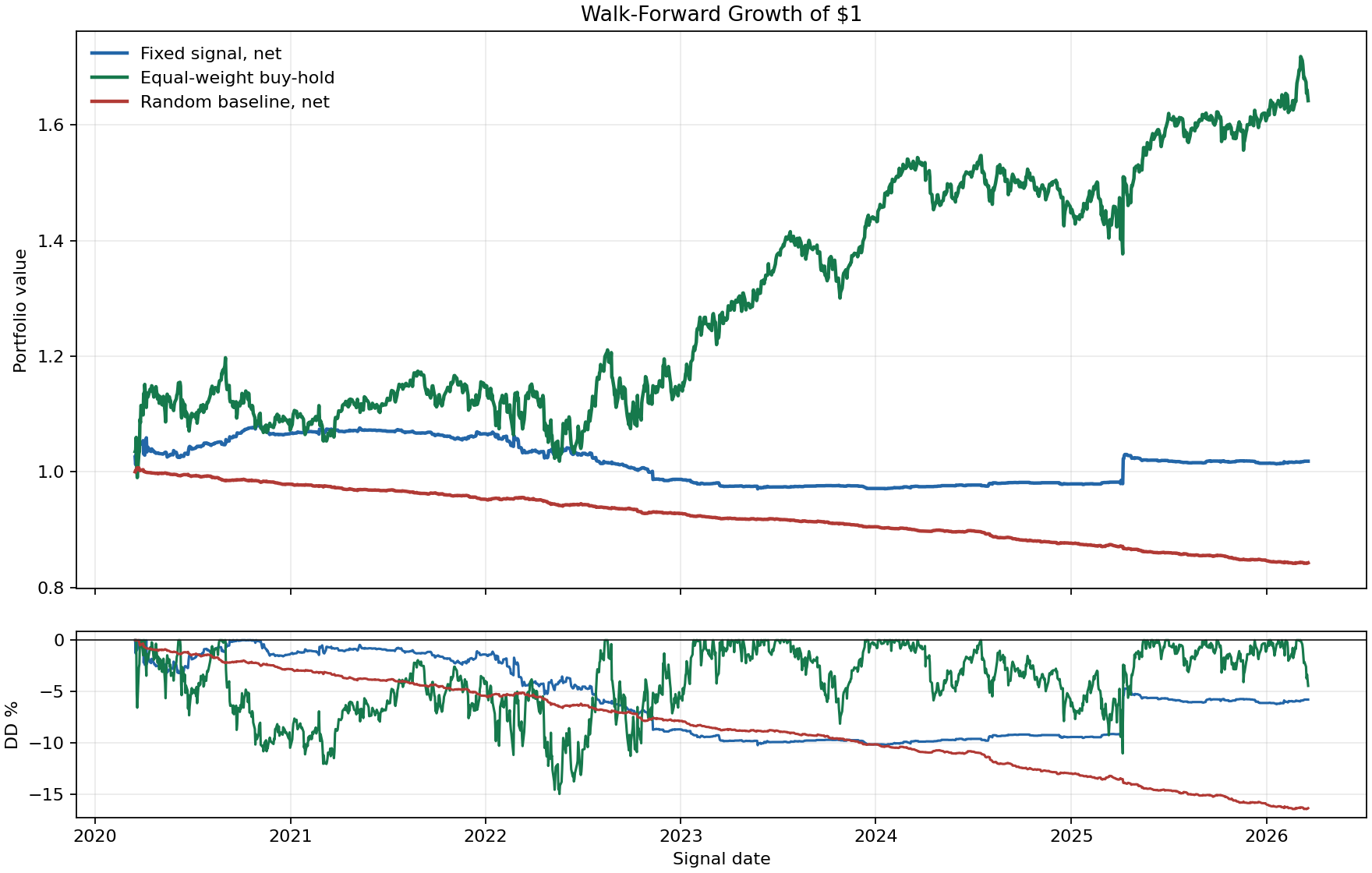

| Method | Total Return | Ann. Sharpe | Max Drawdown | Interpretation |

|---|---|---|---|---|

| Fixed logistic signal, net | +1.84% | 0.097 | -10.21% | Real but tiny; barely positive after costs. |

| Equal-weight buy-hold | +64.20% | 0.646 | -14.95% | Just holding the names wins easily. |

| Zero-skill random, net | -15.74% | -3.499 | -16.42% | Trades at the same rate; shows the cost drag. |

What keeps the test clean

The harness is built to fail the strategy if it can. Every transform is fit inside the training fold, trades lag the signal by a day, and the baselines use the same data the signal does.

StandardScaler is inside the sklearn pipeline and fit only on training slices.| Diagnostic | Value |

|---|---|

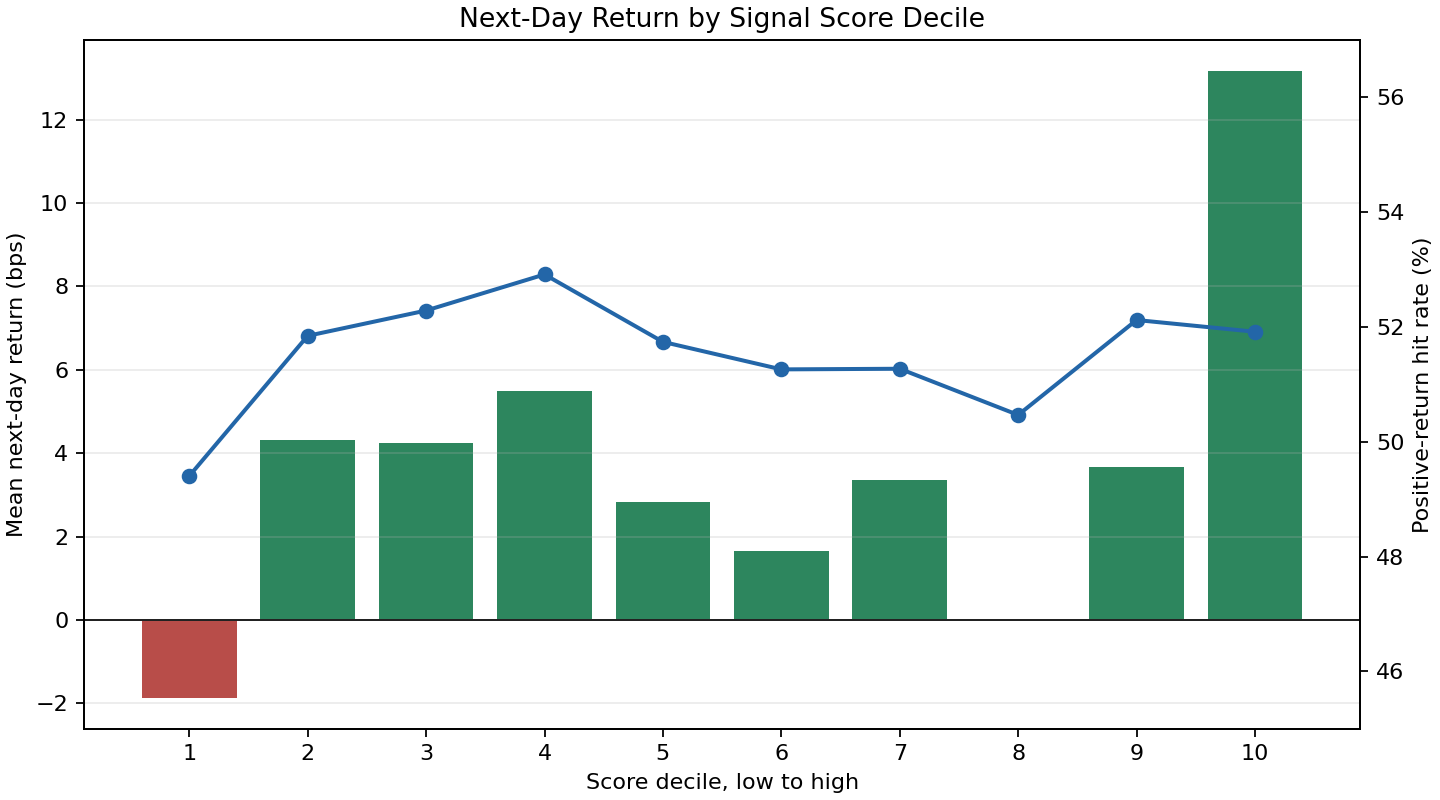

| IC t-stat | 2.19 |

| Active hit rate | 53.47% |

| Active fraction | 5.36% |

| Configuration lower bound | 41 |

| DSR probability | 1.79e-235 |

What the plots show

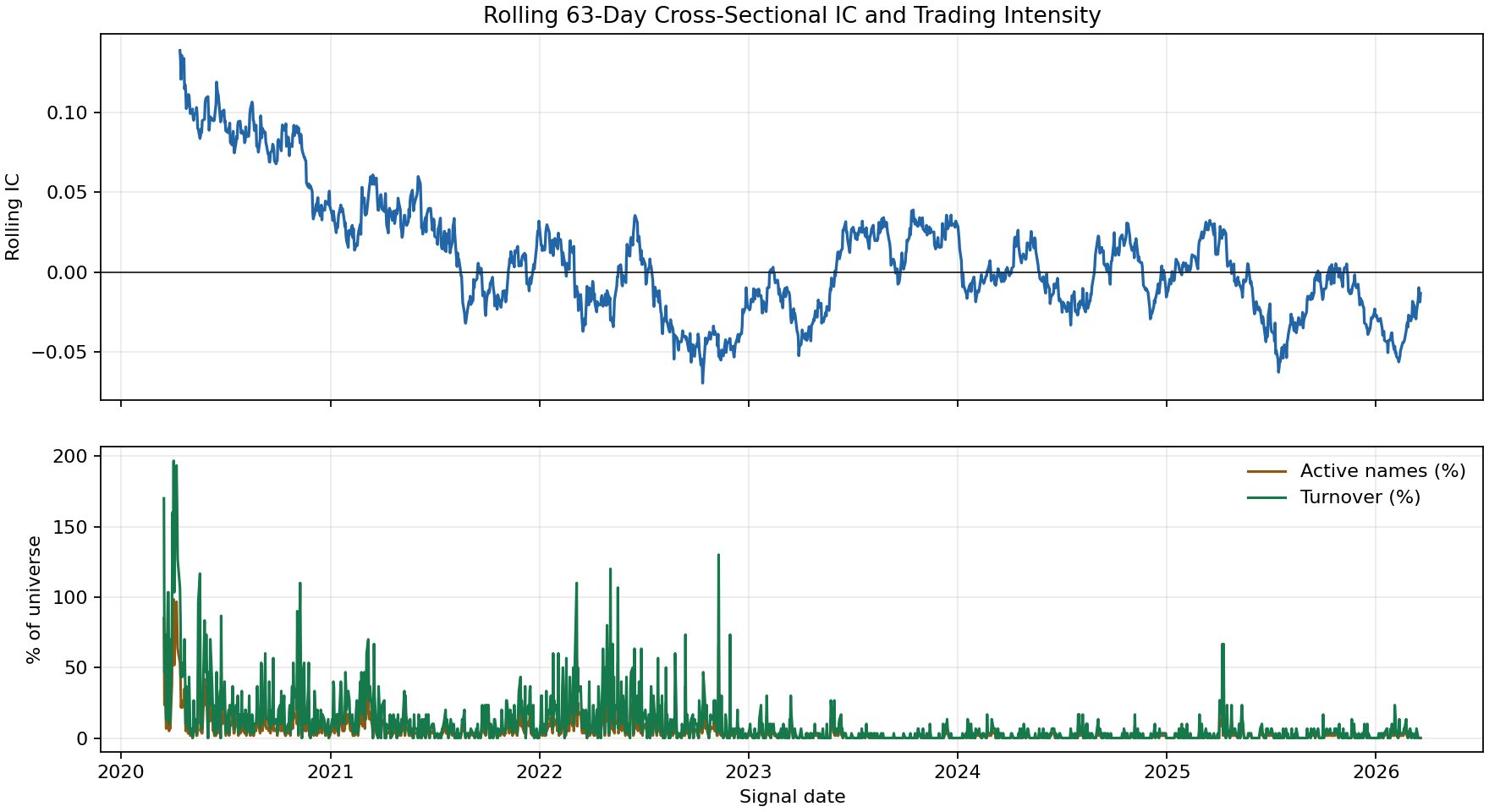

These are the three plots I actually care about: does it beat the baselines, does a higher score mean a higher return, and does the signal hold up over time.

Why the old numbers can't be trusted

I kept the earlier experiments because they show how good-looking metrics come out of a narrow ticker list, same-bar trades, and trying a lot of configs.